DAO Research

Intraday Strategy

Update I - 25/06/2024

Gorn SR scalping Strategy

Concept

incepted by Ryu aka Petar

View on Gitbook:

View Gorn SR scalping v1 trackrecord 2023 here

INDEX

Preface

I. Introduction

II. Chapter 1: The Gorn SR Scalping Algorithm Semantics

III. Chapter 2: The Benefits of Multiple Timeframes and Asset Diversification of the GornSR algo

IV. Chapter 3: The Synergy of Technical Analysis and Neural Networks

V. Chapter 4: Adding Nonlinearity for Robustness

VI. Conclusion

VII. References

Introduction

The Gorn SR scalping algorithm is used within an array of trading algos covering different timeframes and assets, in other words is used within an algorithmic portfolio of scalping algos. This algorithmic scalping portfolio represents a sophisticated approach to algorithmic trading, emphasizing the synergy of multiple technical analysis tools and neural networks. This Gorn SR scalping portfolio, leverages the strengths of various scalping algorithms across different timeframes and assets, aims to optimize trading performance by ensuring robustness, adaptability, and high returns.

The Gorn SR scalping algorithm is used within an array of trading algos covering different timeframes and assets, in other words is used within an algorithmic portfolio of scalping algos. This algorithmic scalping portfolio represents a sophisticated approach to algorithmic trading, emphasizing the synergy of multiple technical analysis tools and neural networks. This Gorn SR scalping portfolio, leverages the strengths of various scalping algorithms across different timeframes and assets, aims to optimize trading performance by ensuring robustness, adaptability, and high returns.

This paper delves into the intricacies of the Gorn SR scalping algorithms, highlighting the benefits of their semantics and the strategic advantage of employing a diversified portfolio of algorithms. We will also discuss the integration of nonlinear dynamics in trading systems, the importance of continuous improvement, and the application of walk-forward analysis to maintain system efficacy.

Chapter 1: The Gorn SR Scalping Algorithm Semantics

The Gorn SR scalping algorithm employs a variety of technical analysis tools, including Fibonacci-based support and resistance pattern analysis, Supertrend indicators, Exponential Moving Averages (EMA), time considerations, daily loss and profit considerations, equity curve control, breakeven stops, trailing stops, and ATR-based profit target stops. Each of these components contributes uniquely to the overall strategy, enhancing its ability to capture profitable trading opportunities while mitigating risks.

1.1 Fibonacci-Based Support and Resistance

Fibonacci retracement levels are crucial in identifying potential reversal points in the market. By integrating Fibonacci levels into the Gorn SR scalping algorithm, traders can anticipate areas where price movements are likely to encounter support or resistance, thus informing entry and exit points. This method, rooted in mathematical ratios, provides a reliable framework for understanding market behavior and enhancing decision-making accuracy.

The Gorn SR scalping algorithm employs a variety of technical analysis tools, including Fibonacci-based support and resistance pattern analysis, Supertrend indicators, Exponential Moving Averages (EMA), time considerations, daily loss and profit considerations, equity curve control, breakeven stops, trailing stops, and ATR-based profit target stops. Each of these components contributes uniquely to the overall strategy, enhancing its ability to capture profitable trading opportunities while mitigating risks.

1.1 Fibonacci-Based Support and Resistance

Fibonacci retracement levels are crucial in identifying potential reversal points in the market. By integrating Fibonacci levels into the Gorn SR scalping algorithm, traders can anticipate areas where price movements are likely to encounter support or resistance, thus informing entry and exit points. This method, rooted in mathematical ratios, provides a reliable framework for understanding market behavior and enhancing decision-making accuracy.

1.2 Supertrend Indicator

The Supertrend indicator is another vital component, offering a straightforward mechanism for identifying the prevailing trend. By providing clear buy and sell signals, the Supertrend indicator simplifies the decision-making process, enabling the algorithm to quickly adapt to changing market conditions and maintain alignment with the dominant trend.

1.3 Exponential Moving Averages (EMA)

EMAs are utilized to smooth out price data and highlight the direction of the trend. The use of multiple EMAs allows the Gorn SR scalping algorithm to capture both short-term and long-term trends, facilitating a more comprehensive analysis of market movements. This layered approach ensures that the algorithm can respond swiftly to emerging trends while maintaining a broader perspective on market dynamics.

Gorn Hegemony DAO is using a custom EMA code, adhering to the code of Gorn culture: adapability.

The Supertrend indicator is another vital component, offering a straightforward mechanism for identifying the prevailing trend. By providing clear buy and sell signals, the Supertrend indicator simplifies the decision-making process, enabling the algorithm to quickly adapt to changing market conditions and maintain alignment with the dominant trend.

1.3 Exponential Moving Averages (EMA)

EMAs are utilized to smooth out price data and highlight the direction of the trend. The use of multiple EMAs allows the Gorn SR scalping algorithm to capture both short-term and long-term trends, facilitating a more comprehensive analysis of market movements. This layered approach ensures that the algorithm can respond swiftly to emerging trends while maintaining a broader perspective on market dynamics.

Gorn Hegemony DAO is using a custom EMA code, adhering to the code of Gorn culture: adapability.

1.4 Time Considerations and Daily Loss/Profit Controls

Time considerations play a pivotal role in the Gorn SR scalping algorithm, dictating the optimal times for entering and exiting trades. By factoring in daily loss and profit controls, the algorithm can enforce discipline and prevent excessive risk-taking. These measures are crucial in maintaining the algorithm's performance over time and protecting the trader's capital.

1.5 Equity Curve Control and Risk Management

Equity curve control mechanisms, such as breakeven stops and trailing stops, are implemented to manage risk and protect profits. Breakeven stops ensure that trades are closed without a loss once a certain profit threshold is reached, while trailing stops lock in profits by adjusting the stop-loss level as the market moves in favor of the trade. Additionally, ATR-based profit target stops are employed to capitalize on volatile market conditions, ensuring maximum profit potential is captured.

Gorn Hegemony DAO developed a custom equity curve management code in EasyLanguage.

Chapter 2: The Benefits of Multiple Timeframes and Asset Diversification of the GornSR algo

The Gorn SR sclaping strategy's use of multiple timeframes and asset diversification offers several advantages, including enhanced robustness, improved risk-adjusted returns, and greater adaptability to market changes.

Time considerations play a pivotal role in the Gorn SR scalping algorithm, dictating the optimal times for entering and exiting trades. By factoring in daily loss and profit controls, the algorithm can enforce discipline and prevent excessive risk-taking. These measures are crucial in maintaining the algorithm's performance over time and protecting the trader's capital.

1.5 Equity Curve Control and Risk Management

Equity curve control mechanisms, such as breakeven stops and trailing stops, are implemented to manage risk and protect profits. Breakeven stops ensure that trades are closed without a loss once a certain profit threshold is reached, while trailing stops lock in profits by adjusting the stop-loss level as the market moves in favor of the trade. Additionally, ATR-based profit target stops are employed to capitalize on volatile market conditions, ensuring maximum profit potential is captured.

Gorn Hegemony DAO developed a custom equity curve management code in EasyLanguage.

Chapter 2: The Benefits of Multiple Timeframes and Asset Diversification of the GornSR algo

The Gorn SR sclaping strategy's use of multiple timeframes and asset diversification offers several advantages, including enhanced robustness, improved risk-adjusted returns, and greater adaptability to market changes.

2.1 Multiple Timeframes

By employing three different timeframes for each asset traded, the GornSR algo portfolio ensures that the algorithms can adapt to various market conditions. This multi-timeframe approach allows for a more nuanced understanding of market trends and dynamics, enabling the algorithms to capture trading opportunities on different timeframes. For instance, short-term timeframes can capture immediate price movements, while longer-term timeframes provide context and confirm broader trends for swing-trade'esque scalp trades, for example the GornSR algo trading Kase 10 bars on the Russel2k futures.

2.2 Asset Diversification

Trading multiple assets, such as the Russell 2000 micro futures (M2K) and the other US indices, across different Kase bar sizes, allows the GornSR algo strategy to leverage the strengths of accessing more trading opportunities. Especially the US market indices exhibit unique characteristics and volatility patterns, and by diversifying across these assets, the strategy can mitigate the impact of adverse market conditions on any single asset. An example would be when investors shift their profits from big tech into small caps (Russel2k) or the Dow (DJIA). This natural selection of the most competitive algorithms across multiple timeframes and assets, smooths out the equity curve and enhances the overall performance of the Gorn algorithm portfolio.

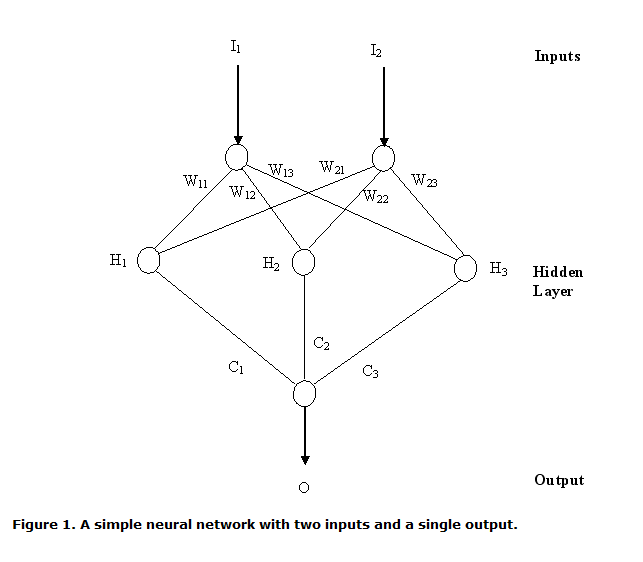

Chapter 3: The Synergy of Technical Analysis and Neural Networks

Integrating technical analysis with neural networks creates a powerful synergy that enhances the Gorn SR scalping strategy's performance. This combination leverages the strengths of both approaches, resulting in a more robust, profitable and adaptive trading system. According to Vanstone and Finnie (2009) a mechanical trading system can be combined with ANNs (artificial neural networks) to enhance market timing and profitability of the system.

3.1 Technical Analysis

Technical analysis provides a structured framework for understanding market behavior based on historical price data and statistical patterns. The use of tools such as Fibonacci retracements and S&R, custom EMAs, and Supertrend indicators allows the algorithm to identify key levels and trends, facilitating precise entry and exit points. Modern technical analysis and the most used indicators, patters and oscillators have been reviewed in Vanstone and Finnie (2009).

3.2 Neural Networks

Neural networks, on the other hand, excel at identifying complex, nonlinear relationships within the data that may not be apparent through traditional technical analysis. By incorporating neural networks, the Gorn SR scalping strategy can enhance its predictive capabilities and adapt to evolving market conditions more effectively. According to Vanstone and Finnie (2009) neural networks are the the cornerstone to bulding a more adaptive and profitable trading system.

By employing three different timeframes for each asset traded, the GornSR algo portfolio ensures that the algorithms can adapt to various market conditions. This multi-timeframe approach allows for a more nuanced understanding of market trends and dynamics, enabling the algorithms to capture trading opportunities on different timeframes. For instance, short-term timeframes can capture immediate price movements, while longer-term timeframes provide context and confirm broader trends for swing-trade'esque scalp trades, for example the GornSR algo trading Kase 10 bars on the Russel2k futures.

2.2 Asset Diversification

Trading multiple assets, such as the Russell 2000 micro futures (M2K) and the other US indices, across different Kase bar sizes, allows the GornSR algo strategy to leverage the strengths of accessing more trading opportunities. Especially the US market indices exhibit unique characteristics and volatility patterns, and by diversifying across these assets, the strategy can mitigate the impact of adverse market conditions on any single asset. An example would be when investors shift their profits from big tech into small caps (Russel2k) or the Dow (DJIA). This natural selection of the most competitive algorithms across multiple timeframes and assets, smooths out the equity curve and enhances the overall performance of the Gorn algorithm portfolio.

Chapter 3: The Synergy of Technical Analysis and Neural Networks

Integrating technical analysis with neural networks creates a powerful synergy that enhances the Gorn SR scalping strategy's performance. This combination leverages the strengths of both approaches, resulting in a more robust, profitable and adaptive trading system. According to Vanstone and Finnie (2009) a mechanical trading system can be combined with ANNs (artificial neural networks) to enhance market timing and profitability of the system.

3.1 Technical Analysis

Technical analysis provides a structured framework for understanding market behavior based on historical price data and statistical patterns. The use of tools such as Fibonacci retracements and S&R, custom EMAs, and Supertrend indicators allows the algorithm to identify key levels and trends, facilitating precise entry and exit points. Modern technical analysis and the most used indicators, patters and oscillators have been reviewed in Vanstone and Finnie (2009).

3.2 Neural Networks

Neural networks, on the other hand, excel at identifying complex, nonlinear relationships within the data that may not be apparent through traditional technical analysis. By incorporating neural networks, the Gorn SR scalping strategy can enhance its predictive capabilities and adapt to evolving market conditions more effectively. According to Vanstone and Finnie (2009) neural networks are the the cornerstone to bulding a more adaptive and profitable trading system.

3.3 Statistical significance

A statistical students T-test was applied to the every single algorithm to once again ensure robustness and expectancy. Moreover, is in-sample testing and AI training based on 20 years price history of the specific asset. Out-of-sample testing was applied on 20 years price history as well as on multiple times, multiple assets. The pinnacle of Gorn is to create the most adaptive trading system, encompassing the most innovative technologies, such as AI and genetic algorithms.

Chapter 4: Adding Nonlinearity for Robustness

Introducing nonlinearity into the Gorn SR scalping portfolio, through the use of neural networks and advanced technical analysis techniques enhances the system's robustness. Nonlinear models can capture more complex market behaviors and interactions, improving the algorithm's ability to predict and respond to market movements.

4.1 Benefits of Nonlinearity

Nonlinear models are better equipped to handle the inherent complexities and uncertainties of financial markets. They can adapt to changing market conditions and identify patterns that linear models might miss. This adaptability is crucial for maintaining the performance of the Gorn SR strategy in a dynamic trading environment.

4.2 Walk-Forward Analysis

Walk-forward analysis is a critical technique for evaluating the robustness and efficacy of the Gorn SR strategy. This method involves continuously updating the model with new data and testing its performance on out-of-sample data. By iterating this process, the algorithm can adapt to changing market conditions and maintain its effectiveness over time.

Conclusion

The Gorn SR scalping portfolio represents a sophisticated and robust approach to algorithmic trading. By integrating multiple technical analysis tools, employing neural networks, and utilizing multiple timeframes and asset diversification, the strategy achieves a high degree of adaptability and performance. The use of nonlinearity and walk-forward analysis further enhances the robustness of the system, ensuring its efficacy in live market conditions. This comprehensive approach to algorithmic trading offers significant advantages, including improved risk-adjusted returns, greater adaptability, and a smoother equity curve.

References

- Kim, K. J., & Shin, K. S. (2007). "A hybrid approach based on neural networks and genetic algorithms for detecting temporal patterns in stock markets." *Applied Soft Computing*, 7(2), 569-576. doi:10.1016/j.asoc.2006.02.001

A statistical students T-test was applied to the every single algorithm to once again ensure robustness and expectancy. Moreover, is in-sample testing and AI training based on 20 years price history of the specific asset. Out-of-sample testing was applied on 20 years price history as well as on multiple times, multiple assets. The pinnacle of Gorn is to create the most adaptive trading system, encompassing the most innovative technologies, such as AI and genetic algorithms.

Chapter 4: Adding Nonlinearity for Robustness

Introducing nonlinearity into the Gorn SR scalping portfolio, through the use of neural networks and advanced technical analysis techniques enhances the system's robustness. Nonlinear models can capture more complex market behaviors and interactions, improving the algorithm's ability to predict and respond to market movements.

4.1 Benefits of Nonlinearity

Nonlinear models are better equipped to handle the inherent complexities and uncertainties of financial markets. They can adapt to changing market conditions and identify patterns that linear models might miss. This adaptability is crucial for maintaining the performance of the Gorn SR strategy in a dynamic trading environment.

4.2 Walk-Forward Analysis

Walk-forward analysis is a critical technique for evaluating the robustness and efficacy of the Gorn SR strategy. This method involves continuously updating the model with new data and testing its performance on out-of-sample data. By iterating this process, the algorithm can adapt to changing market conditions and maintain its effectiveness over time.

Conclusion

The Gorn SR scalping portfolio represents a sophisticated and robust approach to algorithmic trading. By integrating multiple technical analysis tools, employing neural networks, and utilizing multiple timeframes and asset diversification, the strategy achieves a high degree of adaptability and performance. The use of nonlinearity and walk-forward analysis further enhances the robustness of the system, ensuring its efficacy in live market conditions. This comprehensive approach to algorithmic trading offers significant advantages, including improved risk-adjusted returns, greater adaptability, and a smoother equity curve.

References

- Kim, K. J., & Shin, K. S. (2007). "A hybrid approach based on neural networks and genetic algorithms for detecting temporal patterns in stock markets." *Applied Soft Computing*, 7(2), 569-576. doi:10.1016/j.asoc.2006.02.001

- Neely, C. J., Rapach, D. E., Tu, J., & Zhou, G. (2014). "Forecasting the equity risk premium: The role of technical indicators." *Management Science*, 60(7), 1772-1791. doi:10.1287/mnsc.2013.1838

- Vanstone, B. J., & Finnie, G. R. (2009). "An empirical methodology for developing stockmarket trading systems using artificial neural networks." *Expert Systems with Applications*, 36(3), 6668-6680. doi:10.1016/j.eswa.2008.08.005

- Pardo, R. (2012). *The Evaluation and Optimization of Trading Strategies*. John Wiley & Sons.

- Tsinaslanidis, P. E., & Kugiumtzis, D. (2014). "A prediction scheme using hybrid pattern recognition methods." *Expert Systems with Applications*, 41(6), 2793-2806. doi:10.1016/j.eswa.2013.10.036